Prudential Singapore has introduced three new Integrated Shield Plan riders under its PRUExtra Care series, offering broad medical coverage with premiums that are at least 30 percent lower than the previous riders across all age groups and plan types.

The Ministry of Health (MOH) introduced new requirements for Integrated Shield Plan riders to address rising healthcare costs and ensure the long-term sustainability of private health insurance in Singapore. From 1 April 2026, new riders can no longer cover the minimum deductible, and the co-payment cap has been raised to S$6,000, while the 5 per cent co-payment remains. These changes aim to encourage more prudent use of healthcare services, reduce over-consumption and large claims, and refocus insurance on protecting against major medical bills rather than covering all costs.

Any PRUExtra riders purchased between 27 November 2025 and 31 March 2026 will need to move to the new supplementary plans that meet updated requirements, starting from their next policy renewal on or after 1 April 2028.

The new riders include enhanced critical illness coverage and a retrenchment benefit. As conditions such as cancer, heart attack and stroke continue to rise in Singapore, Prudential has introduced an early-to-late critical illness benefit. If a customer is hospitalised or requires surgery for a covered condition, their annual policy limit can increase by up to S$100,000.

For PRUExtra Premier Care and PRUExtra Preferred Care customers, a retrenchment waiver is also available. If they are unemployed for at least six continuous months, they can apply to waive their rider premiums for up to 12 months. The waiver remains in place even if they return to work during that period.

| Product | Where You Can Use It | Key Benefit | What’s New |

|---|---|---|---|

| PRUExtra Premier Care | Private hospitals | Covers more costs with panel doctors | Up to S$100,000 extra cover for critical illness, retrenchment premium waiver. Extra Cover for Early to Late Critical Illness benefit: – PRUExtra Premier Care: $100,000 additional limit per policy year – PRUExtra Preferred Care: $100,000 additional limit per policy year – PRUExtra Plus Care: $50,000 additional limit per policy year |

| PRUExtra Preferred Care | Selected private hospitals (panel list) | Lower premiums with panel use. Premiums are at least 45 percent more affordable across all age groups compared to its previous corresponding rider, with some groups seeing a 55 percent difference. | At least 45% cheaper vs old plan, same S$100,000 critical illness boost |

| PRUExtra Plus Care | Public hospitals (Class A wards) | Lower cost option | Up to S$50,000 extra critical illness cover |

Similar to the previous rider, PRUExtra Premier Care customers who seek treatment from panel or extended panel specialists at approved healthcare institutions can maintain their premium level at the next renewal under the claims-based pricing framework. They also receive a 20 percent PRUWell Reward discount on the standard premium tier when the policy is issued without special terms, and again at renewal if no claims are made.

Comparison of key features in Prudential Singapore’s previous and new riders

| Key features | Previous PRUExtra CoPay riders | New PRUExtra Care riders |

|---|---|---|

| Deductible coverage | Covered, up to 95% | Not covered for the first $3,500. Covers 95% of the deductible amount above $3,500. |

| Co-insurance | Covered, up to 50% | Covered, up to 50% |

| Co-payment cap/ Stop-loss limit | $3,000 | $6,000 |

| Extra cover for early to late critical illness benefit | No | Yes New |

| Retrenchment waiver benefit | No | Yes New • PRUExtra Premier Care • PRUExtra Preferred Care |

| Non-listed cell, tissue, and gene therapy product (CTGTP) | Covered | Covered |

| Non-cancer drug list services and treatments * | Covered | Covered |

| Claims-based premium pricing | Yes • PRUExtra Premier CoPay • PRUExtra Preferred CoPay | Yes • PRUExtra Premier Care |

| Access to PRUPanel Connect ** | Yes • PRUExtra Premier CoPay • PRUExtra Preferred CoPay | Yes • PRUExtra Premier Care • PRUExtra Preferred Care |

* PRUExtra riders (previous and new) provide additional coverage of S$150,000 per annum on non-cancer drug list (CDL) treatments (drug classes A to E) which are outside the scope of standard MediShield Life (MSHL) and IP main plan coverage. PRUExtra customers also get higher coverage of 15x the MSHL limit (monthly limit) for cancer drug treatments listed on the CDL and 15x the MSHL limit (yearly limit) for cancer drug services.

** PRUExtra Premier Care and PRUExtra Preferred Care customers have access to PRUPanel Connect (PPC), Prudential’s hospital partnership programme launched in 2019. Under the PPC programme, they can choose from a wide array of healthcare options for panel specialists and medical specialties, enjoy enhanced convenience from value-added services, and better management of healthcare costs. PPC currently has over 2,000 specialists.

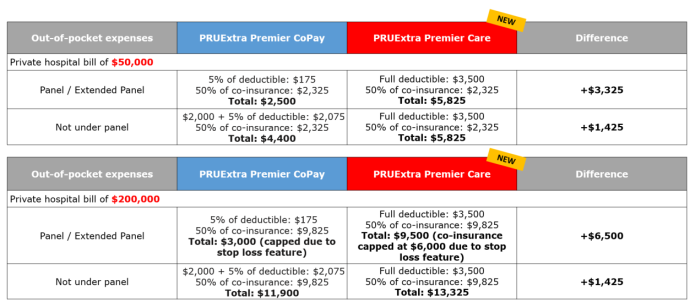

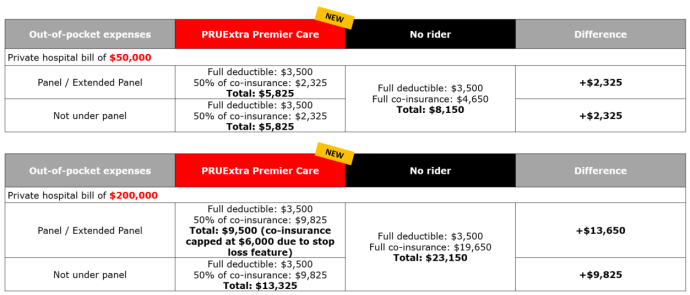

Comparison of Out-of-Pocket Expenses

Out of pocket comparison of Previous vs New PRUExtra riders (Private Hospital Plan)

Out of Pocket expenses comparison of New PRUExtra riders vs No Riders (Private Hospital Plan)

Healthcare needs and financial circumstances vary for individuals. Review your protection with your financial representative to assess your overall needs and determine the appropriate level of coverage before making any decision to downgrade or drop your riders. Customers who already have riders should be aware of the following if they are considering any changes from 1 April 2026:

| Upgrade or downgrade to a withdrawn rider from the previous suite | Not allowed. You can only switch to the new PRUExtra Care series. Ensure that you’re comfortable with the new breadth of coverage and options. |

| Drop rider and keep the existing main plan only | You will have to fully shoulder the co-insurance and forgo the stop-loss benefit. There will no longer be coverage for certain value-added services, including PRUPanel Connect benefits, non-cancer drug list treatments, and non-listed CTGTPs. |

| Switch to a new rider from the PRUExtra Care series | The benefits from your old rider will no longer apply. If it’s an upgrade, the application is subject to medical underwriting and possible exclusions depending on your health situation and underwriting outcome. |